Stablecoin Headlines Generate Attention. Adoption is Another Story.

Stablecoin Field Guide for Corporate and Institutional Adoption #1

Stablecoin transaction headlines generate attention. Institutional adoption, however, is much more difficult.

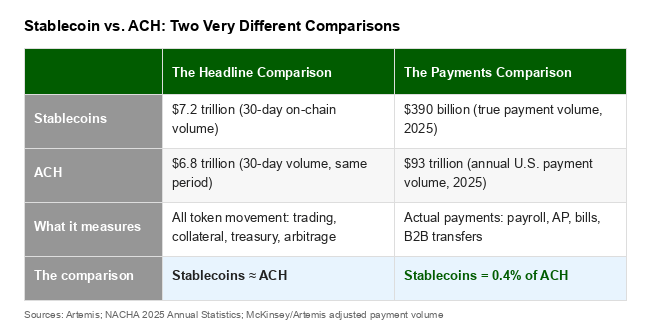

Stablecoins may have just “beaten” ACH on total volume. Once you align the statistics and use cases properly, the story reads more like coexistence than conquest.

Artemis data shows that stablecoins briefly overtook ACH in February, settling about $7.2 trillion in adjusted 30‑day on-chain dollar volume versus roughly $6.8 trillion for ACH over the same period. That’s the eye‑catching news peg behind a wave of LinkedIn, X, and business media articles claiming that stablecoins are overtaking the U.S. financial system’s payments infrastructure.

The problem is that the headlines mismatch what the two systems do in the real economy, the place where the corporate and institutional adoption that matters occurs.

Adoption, Not Attention

I’m not arguing that growth and interest in stablecoins—clearly this year’s model—are unimportant as future infrastructure or lack valid use cases.

I am pointing out that focusing on media headline numbers or the marketing vanity metrics, interesting though they may be, is not a real indicator of product adoption. From a product perspective, it’s a matter of use cases and cost efficiencies. For most U.S. uses, payments are not at the top of the institutional stablecoin list.

Consider the results from the latest Association of Financial Professionals (AFP) digital payments survey. Only 13% of respondents reported that they were “very familiar” or “familiar” with stablecoins. The total increased to 34% for tokenized purchases (money markets, deposits, repo, etc.), underscoring that tokenization of traditional assets is currently ahead of pure stablecoin payments in mindshare.

Stablecoin flows are mostly collateral movements, treasury shifts, and trading infrastructure—call it money movement. ACH flows are one‑off credits and debits tied to corporate accounts payable, salaries, Social Security, mortgages, electric bills, and anything else that people think of when they hear “payments.”

If you isolate payments from raw token movement, the picture changes fast. A recent McKinsey and Artemis analysis puts true stablecoin payment volume at about $390 billion in 2025, after stripping out exchange internal transfers, arbitrage, and smart‑contract noise. That is just 0.02% of global payments volume, with about 60% of stablecoin payments coming from B2B use cases such as cross‑border supplier and treasury flows.

Making a payments-to-payments comparison on $390 billion in global stablecoin payments versus $93 trillion in U.S. ACH payments is where the headlines break down. That’s a long way from “stablecoins are replacing the U.S. payments system” and a misuse of the ACH comparison. There’s a big difference between attention and adoption, especially in corporate and institutional payments.

ACH and Other Bank Payments

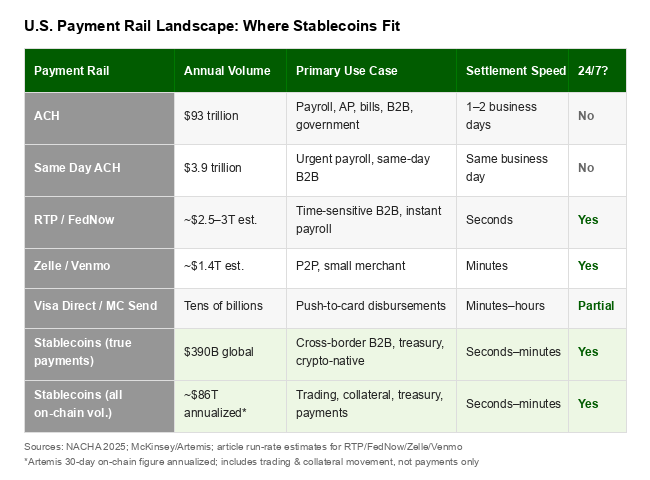

ACH remains the Main Street of U.S. personal, corporate, and government money movement. NACHA’s latest numbers show the network processed 35.2 billion payments in 2025, totaling $93 trillion in value, up 7.9% in value and 4.9% in volume from 2024. Same Day ACH is experiencing a growth spurt, moving $3.9 trillion last year, a growth rate of more than 20%.

Parallel to ACH and card network value exchange systems, U.S. financial institutions—long known for the slow speed of payment rail changes—are building a growing cluster of faster and instant payments: RTP, FedNow, Zelle, Venmo, and card‑based push payments, at current run-rate estimates. They also do what most people think of as “payments” and target specific urgency problems with different volume metrics.

RTP and FedNow together are probably moving on the order of roughly $200–250 billion a month, Zelle and Venmo add maybe another $120 billion in mostly P2P and small‑merchant flows, and Visa Direct/Mastercard Send contribute additional tens of billions globally.*

Looked at that way, faster payments and P2P apps are less an alternative to ACH and more another layer of specialized plumbing. Much like stablecoins, they are designed to handle time‑sensitive or cross‑platform use cases while the ACH network continues to function as the core domestic payments backbone, alongside check and cash. (Both checks and cash are shrinking in usage, but likely not as fast as you think they should.)

Again, the problems and volumes need to be aligned with the appropriate use cases for the many available U.S. payment solutions.

Whither Stablecoins and Tokenization?

Traditional payments and digital finance are starting to converge in bank‑issued tokens like Societe Generale‑FORGE’s USD CoinVertible. SocGen has now integrated its fully reserved USD stablecoin into MetaMask via a ConsenSys partnership, making a MiCA‑compliant bank dollar available to millions of self‑custody wallet users and thousands of dApps.

As Bloomberg reported: “Stablecoins enable faster, programmable and more efficient transfers of value while maintaining price stability,” Jean-Marc Stenger, Societe Generale-FORGE chief executive officer, said in an interview. “From a banking perspective, stablecoins also provide a way to bring traditional strengths—risk management, compliance, transparency, and governance—into blockchain‑based systems.”

As another recent example, Northern Trust Co., in its first quarter 2026 earnings call, noted that it onboarded new digital asset clients providing custody for tokenized real-world assets, U.S. stablecoins, and carbon credits. The custody bank also launched a tokenized share class to broaden global liquidity vehicles.

“By applying tokenization to institutional-grade liquidity strategies, we’re offering clients a modern, digital-first way to access money market investments while maintaining our high standards for risk management and service,” said Northern Trust CEO Mike O’Grady on the earnings call.

These are real corporate and institutional use cases where digital assets meet needs that traditional payments rails handle poorly. SocGen is taking a fully reserved, bank‑regulated dollar token and aiming it squarely at the inefficiencies in institutional and cross‑border systems.

“Better-faster-cheaper” bank product analyses will turn up others. This looks more like a bridge than a rebellion: regulated bank money wrapped for programmable, 24/7 settlement in markets and B2B flows where ACH never fit well.

The LinkedIn and X celebrations get the direction of travel right—stablecoins are becoming serious financial infrastructure—but their misuse of the ACH comparison obscures where real institutional adoption is happening, how many alternatives are developing, and how far any payments innovation has to go to compete seriously.

In my U.S. Payments Timeline, I have marked early 2026 as the point where the stablecoin and tokenized‑deposit showdown starts to get real, with Artemis’s “stablecoins beat ACH” chart sitting alongside new FDIC GENIUS Act rules and bank‑issued dollar tokens.

Seen through that lens, the ACH comparison is less a changing‑of‑the‑guard moment and more an early sign of convergence—multiple flavors of digital dollars learning to share the same payment stack. If there is a cypherpunk “killer app” here, it’s not killing ACH; it’s making the dollar programmable and globally accessible.

That, in itself, has become a point of coexistence rather than conquest. As Aaron Brown wrote in a Bloomberg Opinion, news-pegged to the ACH metrics:

“The cypherpunks foresaw all of these use cases with remarkable precision: frictionless cross-border settlement, aid disbursement without intermediaries, complex multi-currency transactions handled cleanly. They just assumed the underlying unit of account would be something anarchic and stateless. It is, instead, the currency of the United States federal government. Big brother.”

*Perplexity calculated these estimates for me. If you want to know how, send me a note.

Selected Bibliography

Aaron Brown, “The Cypherpunks Wanted to Destroy the Dollar. They Saved It Instead,” Bloomberg Opinion, April 15, 2026.

Anna Irrera, “SocGen Takes USD Stablecoin to Millions of Crypto Wallet Users,” Bloomberg, April 15, 2026.

Artemis data summarized in CoinMarketCap and others, “Stablecoins Surpass ACH Volume for the First Time,” April 2, 2026; “Stablecoin Transactions Surpass ACH Volume in February.”

Association of Financial Professionals (AFP), “2025 AFP Digital Payments Survey.”

IntelliPay, “ACH Payment Volume Hit 93 Trillion in 2025 – What the Record-Breaking Numbers Mean for Businesses and Government,” February 1, 2026.

McKinsey / Artemis, “Stablecoin Payments Surge to $390 Billion in 2025” and “Stablecoins in payments: What the raw transaction numbers miss,” February 2026

NACHA, “ACH Network Volume and Value Statistics”; “Same Day ACH and Business-to-Business Payments Propel ACH Network Volume Growth in 2025”; “ACH Network Sees Strong Start to 2025; Volume and Value Increases.”

Northern Trust Co., Q1 2026 Earnings Call, April 21, 2026.

Payments Dive, “Stablecoins Remain Little Used for Payments,” April 13, 2026.